Insurance contract management: Carrier and broker use cases

Insurance contract management: Carrier and broker use cases

Insurance contract management: Carrier and broker use cases

Insurance contract management: Carrier and broker use cases

contract management

Key takeaways

Insurance runs on layered, multi-party agreements (policies, treaties, carrier appointments, producer contracts) that spreadsheets cannot model without losing the relationships that carry financial and regulatory weight.

Missed deadlines are categorically higher-stakes here: a lapsed appointment can end binding authority, a lapsed certificate creates coverage gaps, and a missed treaty leaves catastrophic exposure unhedged.

Carriers need tiered approval routing and examinable audit trails. Brokers and MGAs need appointment, binding-authority, and commission-schedule visibility.

AI data extraction turns a months-long migration of existing contracts into a job of days.

Adoption depends on low friction: external parties access by email link and redline in Word or Google Docs, with no new accounts.

Insurance organizations run on contracts. Every policy, every carrier appointment, every reinsurance treaty, every producer agreement represents a binding obligation with deadlines, authority limits, and regulatory implications. Yet many carriers and brokers still manage these agreements through email threads, shared drives, and spreadsheets that buckle under the weight of a complex insurance contract portfolio.

Effective insurance contract management requires more than a digital filing cabinet. It demands a system built around the realities of how insurance agreements actually work: layered documents, multi-party relationships, certificate-of-insurance tracking, conditional approval routing, and audit trails that satisfy state regulators.

This post breaks down what makes insurance contract portfolios uniquely challenging and how carriers and brokers can address those challenges with a purpose-built contract lifecycle management (CLM) approach.

Why insurance contract portfolios demand specialized management

A commercial SaaS company might manage three or four contract types. An insurance carrier manages dozens: producer agreements, reinsurance treaties, MGA contracts, vendor agreements, surplus lines brokerage agreements, employment contracts, and more. Each type carries its own approval authorities, regulatory requirements, and renewal cadences.

Brokers face a parallel complexity. They manage carrier appointment letters, binding authority agreements, commission schedules, client service agreements, and errors-and-omissions coverage contracts. A single carrier relationship might involve five or more linked documents with cross-references that affect how each one should be interpreted.

Carrier | Broker / MGA | |

|---|---|---|

Core agreements | Producer agreements, reinsurance treaties, MGA and vendor contracts | Carrier appointments, binding authority, commission schedules |

Top risk | Authority breaches and adverse audit findings | A missed appointment renewal that ends placement ability |

Key capability | Tiered approval routing, audit trails | Renewal alerts, commission tracking, clause library |

This structural diversity is the core reason spreadsheet-based tracking fails for insurance organizations. You cannot flatten a hierarchical, multi-layered contract portfolio into rows and columns without losing the relationships between documents, and those relationships carry real financial and regulatory consequences.

The cost of missed deadlines in insurance

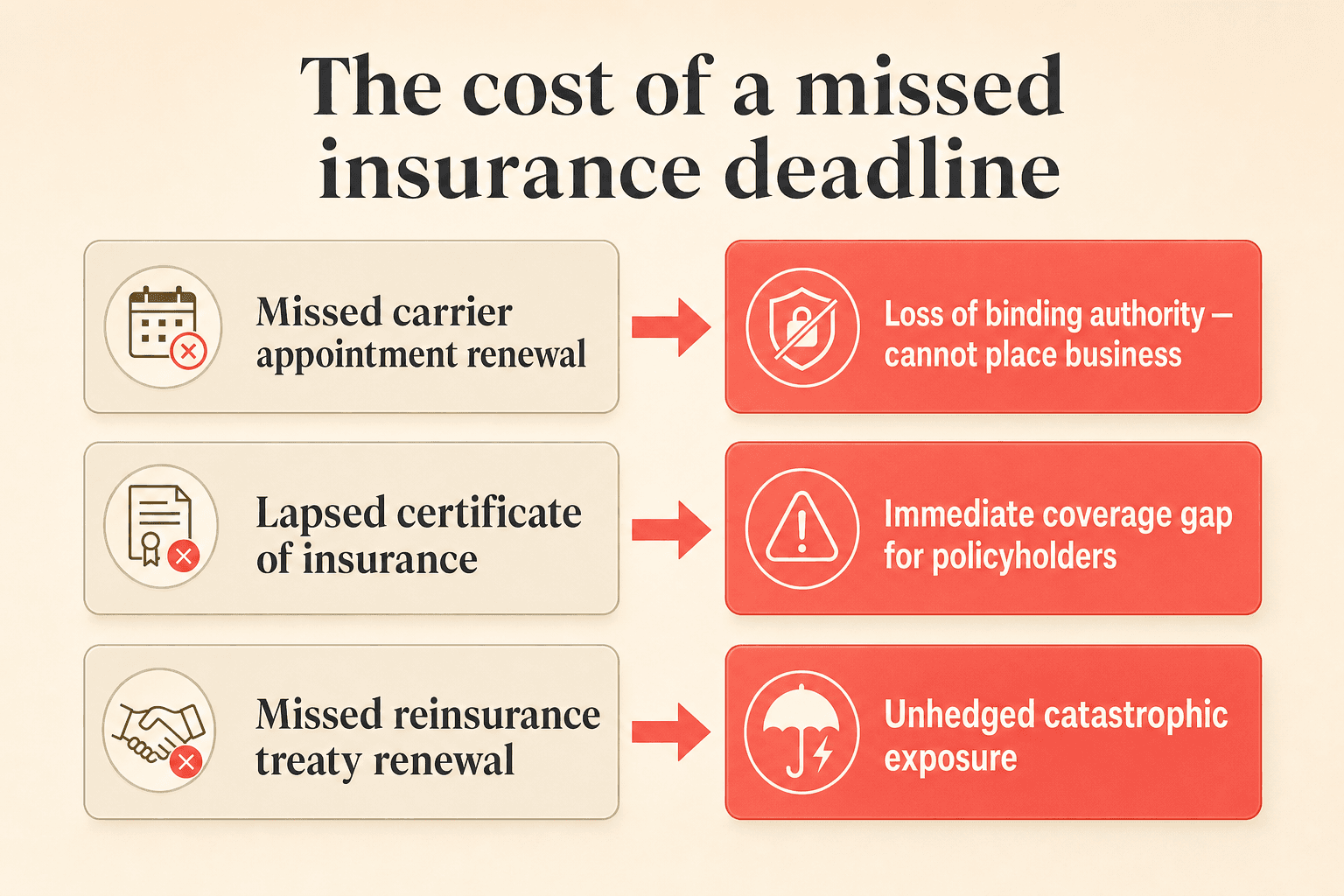

In most industries, a missed contract renewal triggers an inconvenient renegotiation. In insurance, the stakes are categorically different.

A missed renewal on a carrier appointment can mean loss of binding authority, leaving a brokerage unable to place business with that carrier. A lapsed certificate of insurance can create immediate coverage gaps for policyholders. A missed reinsurance treaty renewal can leave a carrier holding unhedged catastrophic exposure.

Contract administrators at insurance organizations frequently describe deep anxiety about these deadlines, particularly when tracking depends on a single person's institutional knowledge. When that person retires or leaves, the entire deadline management system walks out the door with them.

A proper contract deadline management system addresses this by creating automated alerts with configurable notification windows (30, 60, or 90 days before expiration), weekly email digests of upcoming deadlines, and calendar sync to Outlook or Google Calendar. Certificate-of-insurance expirations, reinsurance treaty renewals, carrier appointment windows, and regulatory filing deadlines can each be tracked as separate custom deadlines, independent of the main agreement's lifecycle.

Insurance contract management for carriers

Carriers face a distinct set of contract management challenges rooted in their role as risk-bearing entities subject to direct regulatory oversight.

Tiered authority limits and approval routing

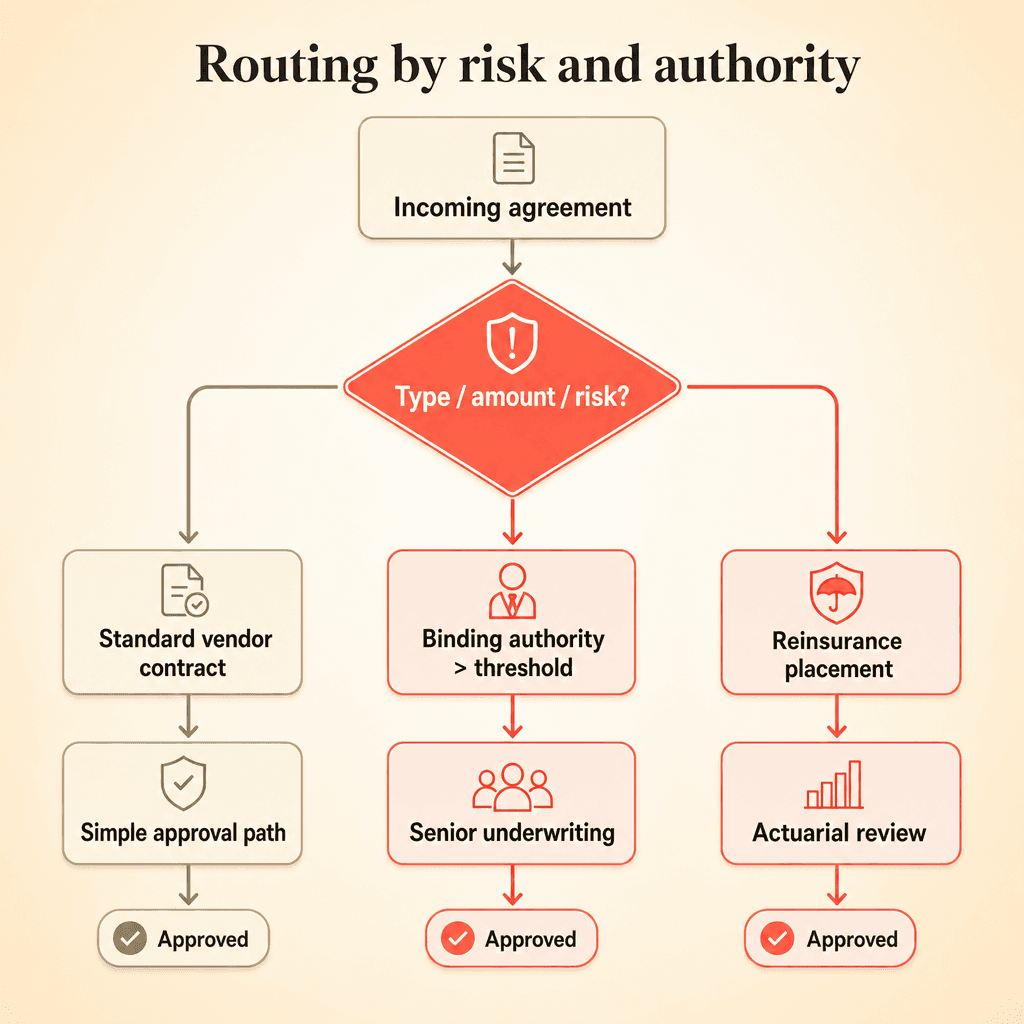

Underwriting authority isn't uniform across a carrier's organization. A junior underwriter might bind risks up to a certain threshold, while larger or more complex risks require senior underwriting approval, actuarial review, or reinsurance sign-off. These authority tiers need to be reflected in how contracts move through approval.

Conditional approval workflows make this possible by routing contracts differently based on type, dollar amount, or risk classification. A binding authority agreement above a certain threshold routes automatically to senior underwriting. A reinsurance placement routes to actuarial review. A standard vendor contract follows a simpler path. The system mirrors the carrier's actual authority structure rather than forcing every agreement through the same pipeline.

Regulatory audit readiness

State insurance departments conduct market conduct examinations. Surplus lines carriers face compliance reviews. In each case, examiners expect to see who approved a contract, when terms changed, and whether the organization followed its own authority limits.

Email threads and shared drives don't produce examinable records. Built-in audit trails, version history, and approval workflow tracking create the documentary evidence that regulatory examinations require, without the manual reconstruction that eats weeks of staff time before an audit.

Reinsurance contract management

Reinsurance treaties are among the most complex agreements a carrier manages. They involve specialized terminology, layered coverage structures, and financial terms that interact with the carrier's overall risk profile. Extracting key terms from these agreements manually is time-consuming and error-prone.

AI-powered data extraction can automatically pull parties, lifecycle dates, financial terms, and custom insurance-specific data points (coverage limits, authority thresholds, commission rates) from uploaded contracts. This turns what would be months of manual cataloging during a system migration into a bulk-upload process.

Insurance contract management for brokers and MGAs

Brokers and managing general agents face different pressures than carriers, but the underlying contract management challenges are equally acute.

Carrier appointment and binding authority tracking

A mid-sized brokerage might hold appointments with 30 or more carriers, each with its own renewal date, binding authority scope, and commission schedule. Tracking these appointments in a spreadsheet works until it doesn't, and the failure mode is a missed renewal that costs the brokerage its ability to place business with a key carrier.

Broker contract management starts with visibility: knowing what's expiring and when. Many brokers describe this as their entry-point problem before expanding into full lifecycle management. A centralized contract repository with automated renewal alerts provides that visibility without requiring a complete process overhaul on day one.

Commission schedule management

Commission rates vary by carrier, by line of business, and often by production tier. A single carrier relationship might involve multiple commission schedules that change over time through amendments. Keeping track of current commission rates across dozens of carrier relationships is a data management challenge that compounds as the brokerage grows.

Custom property fields allow brokers to tag each agreement with commission percentages, production tiers, and line-of-business classifications, creating a searchable, reportable database of financial terms across the entire carrier portfolio.

Producer agreement consistency

Brokerages that appoint sub-producers need standardized language across their producer agreements, particularly around indemnification, errors-and-omissions requirements, and termination provisions. A clause library with pre-approved insurance language (subrogation waivers, additional insured provisions, E&O requirements) keeps these agreements consistent without requiring legal review of every new appointment.

Overcoming the implementation barrier

Insurance teams frequently express resistance to CLM tools that require significant training or process change. The practical reality is that underwriters, producers, and administrative staff won't adopt a system that's harder than their current email workflow, even if the current workflow is objectively broken.

This resistance is reasonable. Insurance professionals are focused on placing and servicing business, not learning new software. Any system that expects external counterparties to create accounts, learn a new interface, or abandon their preferred editing tools will face adoption failure.

External parties should be able to access contracts via email link without creating accounts. Word and Google Docs compatibility means counterparties can redline in whatever tool they already use. The goal is to reduce friction for both internal users and external trading partners, not add another layer of technology to an already complex process.

Eliminating the manual data entry bottleneck

The biggest barrier to moving from spreadsheets to a CLM isn't cost or complexity. It's the migration itself. Insurance organizations sitting on hundreds or thousands of existing contracts face a daunting cataloging challenge: every agreement needs its key terms extracted and entered into the new system.

AI data extraction changes this math dramatically. Upon upload, the system automatically identifies agreement category, parties, lifecycle details (signed date, effective date, duration, renewal terms, early termination provisions), and financial terms. Custom field extraction handles insurance-specific data points like coverage limits, commission percentages, surplus lines tax obligations, and regulatory filing requirements.

This turns a months-long manual data entry project into something a team can accomplish in days.

Building reports that matter for insurance operations

Once contract data is centralized and structured, reporting becomes possible in ways that spreadsheets can't support. Insurance-specific reports might include:

Expiring carrier appointments by renewal date

Outstanding renewals by line of business

Financial exposure by counterparty

Contracts approaching regulatory filing deadlines

Certificates of insurance lapsing in the next 30 days

These reports can be exported to Excel or generated through an AI co-pilot using natural language queries, putting contract intelligence directly in the hands of the people who need it.

Key takeaways

Insurance runs on layered, multi-party agreements (policies, treaties, carrier appointments, producer contracts) that spreadsheets cannot model without losing the relationships that carry financial and regulatory weight.

Missed deadlines are categorically higher-stakes here: a lapsed appointment can end binding authority, a lapsed certificate creates coverage gaps, and a missed treaty leaves catastrophic exposure unhedged.

Carriers need tiered approval routing and examinable audit trails. Brokers and MGAs need appointment, binding-authority, and commission-schedule visibility.

AI data extraction turns a months-long migration of existing contracts into a job of days.

Adoption depends on low friction: external parties access by email link and redline in Word or Google Docs, with no new accounts.

Insurance organizations run on contracts. Every policy, every carrier appointment, every reinsurance treaty, every producer agreement represents a binding obligation with deadlines, authority limits, and regulatory implications. Yet many carriers and brokers still manage these agreements through email threads, shared drives, and spreadsheets that buckle under the weight of a complex insurance contract portfolio.

Effective insurance contract management requires more than a digital filing cabinet. It demands a system built around the realities of how insurance agreements actually work: layered documents, multi-party relationships, certificate-of-insurance tracking, conditional approval routing, and audit trails that satisfy state regulators.

This post breaks down what makes insurance contract portfolios uniquely challenging and how carriers and brokers can address those challenges with a purpose-built contract lifecycle management (CLM) approach.

Why insurance contract portfolios demand specialized management

A commercial SaaS company might manage three or four contract types. An insurance carrier manages dozens: producer agreements, reinsurance treaties, MGA contracts, vendor agreements, surplus lines brokerage agreements, employment contracts, and more. Each type carries its own approval authorities, regulatory requirements, and renewal cadences.

Brokers face a parallel complexity. They manage carrier appointment letters, binding authority agreements, commission schedules, client service agreements, and errors-and-omissions coverage contracts. A single carrier relationship might involve five or more linked documents with cross-references that affect how each one should be interpreted.

Carrier | Broker / MGA | |

|---|---|---|

Core agreements | Producer agreements, reinsurance treaties, MGA and vendor contracts | Carrier appointments, binding authority, commission schedules |

Top risk | Authority breaches and adverse audit findings | A missed appointment renewal that ends placement ability |

Key capability | Tiered approval routing, audit trails | Renewal alerts, commission tracking, clause library |

This structural diversity is the core reason spreadsheet-based tracking fails for insurance organizations. You cannot flatten a hierarchical, multi-layered contract portfolio into rows and columns without losing the relationships between documents, and those relationships carry real financial and regulatory consequences.

The cost of missed deadlines in insurance

In most industries, a missed contract renewal triggers an inconvenient renegotiation. In insurance, the stakes are categorically different.

A missed renewal on a carrier appointment can mean loss of binding authority, leaving a brokerage unable to place business with that carrier. A lapsed certificate of insurance can create immediate coverage gaps for policyholders. A missed reinsurance treaty renewal can leave a carrier holding unhedged catastrophic exposure.

Contract administrators at insurance organizations frequently describe deep anxiety about these deadlines, particularly when tracking depends on a single person's institutional knowledge. When that person retires or leaves, the entire deadline management system walks out the door with them.

A proper contract deadline management system addresses this by creating automated alerts with configurable notification windows (30, 60, or 90 days before expiration), weekly email digests of upcoming deadlines, and calendar sync to Outlook or Google Calendar. Certificate-of-insurance expirations, reinsurance treaty renewals, carrier appointment windows, and regulatory filing deadlines can each be tracked as separate custom deadlines, independent of the main agreement's lifecycle.

Insurance contract management for carriers

Carriers face a distinct set of contract management challenges rooted in their role as risk-bearing entities subject to direct regulatory oversight.

Tiered authority limits and approval routing

Underwriting authority isn't uniform across a carrier's organization. A junior underwriter might bind risks up to a certain threshold, while larger or more complex risks require senior underwriting approval, actuarial review, or reinsurance sign-off. These authority tiers need to be reflected in how contracts move through approval.

Conditional approval workflows make this possible by routing contracts differently based on type, dollar amount, or risk classification. A binding authority agreement above a certain threshold routes automatically to senior underwriting. A reinsurance placement routes to actuarial review. A standard vendor contract follows a simpler path. The system mirrors the carrier's actual authority structure rather than forcing every agreement through the same pipeline.

Regulatory audit readiness

State insurance departments conduct market conduct examinations. Surplus lines carriers face compliance reviews. In each case, examiners expect to see who approved a contract, when terms changed, and whether the organization followed its own authority limits.

Email threads and shared drives don't produce examinable records. Built-in audit trails, version history, and approval workflow tracking create the documentary evidence that regulatory examinations require, without the manual reconstruction that eats weeks of staff time before an audit.

Reinsurance contract management

Reinsurance treaties are among the most complex agreements a carrier manages. They involve specialized terminology, layered coverage structures, and financial terms that interact with the carrier's overall risk profile. Extracting key terms from these agreements manually is time-consuming and error-prone.

AI-powered data extraction can automatically pull parties, lifecycle dates, financial terms, and custom insurance-specific data points (coverage limits, authority thresholds, commission rates) from uploaded contracts. This turns what would be months of manual cataloging during a system migration into a bulk-upload process.

Insurance contract management for brokers and MGAs

Brokers and managing general agents face different pressures than carriers, but the underlying contract management challenges are equally acute.

Carrier appointment and binding authority tracking

A mid-sized brokerage might hold appointments with 30 or more carriers, each with its own renewal date, binding authority scope, and commission schedule. Tracking these appointments in a spreadsheet works until it doesn't, and the failure mode is a missed renewal that costs the brokerage its ability to place business with a key carrier.

Broker contract management starts with visibility: knowing what's expiring and when. Many brokers describe this as their entry-point problem before expanding into full lifecycle management. A centralized contract repository with automated renewal alerts provides that visibility without requiring a complete process overhaul on day one.

Commission schedule management

Commission rates vary by carrier, by line of business, and often by production tier. A single carrier relationship might involve multiple commission schedules that change over time through amendments. Keeping track of current commission rates across dozens of carrier relationships is a data management challenge that compounds as the brokerage grows.

Custom property fields allow brokers to tag each agreement with commission percentages, production tiers, and line-of-business classifications, creating a searchable, reportable database of financial terms across the entire carrier portfolio.

Producer agreement consistency

Brokerages that appoint sub-producers need standardized language across their producer agreements, particularly around indemnification, errors-and-omissions requirements, and termination provisions. A clause library with pre-approved insurance language (subrogation waivers, additional insured provisions, E&O requirements) keeps these agreements consistent without requiring legal review of every new appointment.

Overcoming the implementation barrier

Insurance teams frequently express resistance to CLM tools that require significant training or process change. The practical reality is that underwriters, producers, and administrative staff won't adopt a system that's harder than their current email workflow, even if the current workflow is objectively broken.

This resistance is reasonable. Insurance professionals are focused on placing and servicing business, not learning new software. Any system that expects external counterparties to create accounts, learn a new interface, or abandon their preferred editing tools will face adoption failure.

External parties should be able to access contracts via email link without creating accounts. Word and Google Docs compatibility means counterparties can redline in whatever tool they already use. The goal is to reduce friction for both internal users and external trading partners, not add another layer of technology to an already complex process.

Eliminating the manual data entry bottleneck

The biggest barrier to moving from spreadsheets to a CLM isn't cost or complexity. It's the migration itself. Insurance organizations sitting on hundreds or thousands of existing contracts face a daunting cataloging challenge: every agreement needs its key terms extracted and entered into the new system.

AI data extraction changes this math dramatically. Upon upload, the system automatically identifies agreement category, parties, lifecycle details (signed date, effective date, duration, renewal terms, early termination provisions), and financial terms. Custom field extraction handles insurance-specific data points like coverage limits, commission percentages, surplus lines tax obligations, and regulatory filing requirements.

This turns a months-long manual data entry project into something a team can accomplish in days.

Building reports that matter for insurance operations

Once contract data is centralized and structured, reporting becomes possible in ways that spreadsheets can't support. Insurance-specific reports might include:

Expiring carrier appointments by renewal date

Outstanding renewals by line of business

Financial exposure by counterparty

Contracts approaching regulatory filing deadlines

Certificates of insurance lapsing in the next 30 days

These reports can be exported to Excel or generated through an AI co-pilot using natural language queries, putting contract intelligence directly in the hands of the people who need it.

Need to know

Frequently Asked Questions

Take the "management" out

of contract management.

Customer Support

Legal

Compare

Resources

Customer Support

Company

Legal

Compare

Resources

Customer Support

Company

Legal

Compare

© 2025 Concord. All rights reserved.